Waste Management & Recycling Sector warns: Proposed Fuel-use Exempt Approach and Definition Changes Detrimental to EU Recycling

In the upcoming weeks, the Member States and the European Commission will decide about rules for calculating recycled content in plastics through a mass balance approach under the Single Use Plastics (SUP) Directive.

This legislation is pivotal in influencing market dynamics and shaping the industry’s trajectory for decades. It will determine the fate of technologies and solutions, either thriving or becoming obsolete. As the inaugural regulation on calculating recycled content from chemical recycling at the European level, this implementing act is poised to serve as a blueprint for future regulations in Europe, including PPWR and ESPR.

The undersigned organisations, representing the full extent of the European waste management and recycling sector, reject both:

- The amendment to the definition of post-consumer plastic waste which, understandably, includes waste generated from plastic products placed on the market of a Member State or of a third country. Such an amendment to the very spirit and letter of the SUP Directive is a substantial change which shall not be made through an implementing decision but through an amendment to the SUP Directive itself, to safeguard the democratic scrutiny it requires;

- The fuel-use exempt allocation model which runs counter to the environmental objectives enshrined in the SUP Directive and will send the wrong signal to the waste management and recycling industry. Before such a model is chosen, an impact assessment is urgently required to precisely assess its environmental and socio-economic impacts.

- It will distort the actual recycled content, contradicting the growing demand for transparency in the consumer market as advocated by the public opinion and government policies. This model would enable companies to claim recycled plastic credits (and content) even if a significant part of the recycled input of the production process goes into other substances and materials that are not processed into plastics.

- There will be a risk of greenwashing accusations, triggering public backlash against the entire recycling sector.

- It will allow manufacturers to maximize profits from existing operations designed for processing fossil fuels, limiting their capacity to accept higher amounts of recycled feedstock. The petrochemical industry achieves high recycled content with minimal plastic waste-derived pyrolysis oil, hindering its transition away from fossil-based plastic.

- It will create an uneven playing field for manufacturers and recyclers already utilizing 100% plastic waste as feedstock, allowing claims of green premium and cost advantage.

- It will facilitate the development of technologies which have a higher environmental and energy footprint than mechanical recycling, thus the urgent need to set up harmonised sustainability criteria that can support technologies with a lower carbon footprint[1].

- There will be a foreseeable diversion of mechanical recyclable waste feedstock to chemical recycling, that needs larger volumes of high-quality input materials.

A viable solution would involve ensuring that for streams where mechanical recycling already enables polymers recycling and meeting recycled content targets, mass balance accounting with attribution cannot be applied. This upholds an approach that is technologically neutral and mindful of environmental impacts. In essence, when there is competition between mechanical and chemical recycling processes, the calculation method for chemical recycling shall not be based on the fuel-use exempt calculation method but another methodology, such as the rolling average. This is particularly relevant for recycled PET under SUP, which is already being mechanically recycled at scale today.

When there is no competition and chemical recycling can offer solutions to plastics currently not recycled, a more lenient mass balance approach could be adopted to ensure investments will be directed towards these waste streams.

Such an approach would ensure that mechanical and chemical recycling are truly complementary and result in the most optimal solution from both environmental and industrial standpoints.

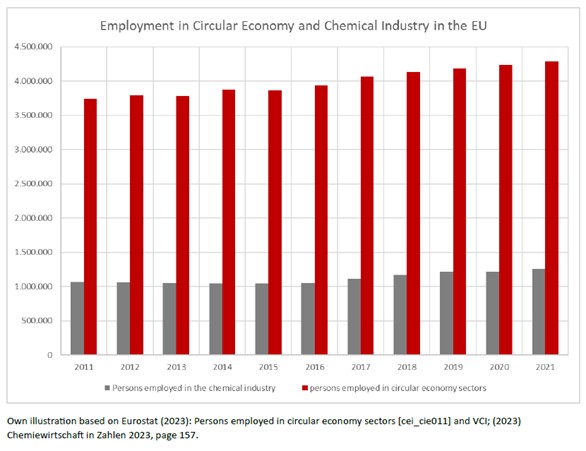

As depicted in the graph below, the circular economy sector already accounts today for many more jobs than the chemical sector. While all economic sectors are important for a vibrant European economy, these local jobs will be endangered if the fuel-use excluded method directs investments towards suboptimal recycling options, potentially creating the conditions for the chemical industry to be dominant. This scenario is all the more unfortunate, considering that many mechanical plastics recyclers are SMEs, often family-owned, which have invested in good faith in the most circular and climate-efficient recycling solution.

In contrast, there are others MBA models which are more suitable to the desired objective and would:

- Allow the necessary investment to develop all the different chemical recycling technologies, creating the right conditions for a neutral technology approach;

- Promote investment for research and technology development to increase the recycled/virgin ratios these plants can handle (that today is still very low)

- Create a level playing field among the different recycling technologies (also for those manufactures and recyclers who already use 100% plastic waste as feedstock)

- Fairly distribute recycled content among the different outputs (polymers, chemicals, fuels and energy), creating the circular economy market conditions for each of them (also for non-plastic output streams of a steam cracker)

[1] To give a practical example: The CO2 emissions of the most common chemical recycling method, the pyrolysis process, are many times higher than the CO2 emissions associated with the mechanical processing of plastic waste into new plastic granulate[1]. In addition, chemical recycling has a significantly lower output in relation to the input than mechanical recycling (see in particular Öko-Institut, Climate impact of pyrolysis of waste plastic packaging in comparison with reuse and mechanical recycling, 2022, page 13 (based on studies by Sphera Solutions GmbH, inter alia for BASF, 2022 and 2020).

The European Recycling Industries’ Confederation (EuRIC) is the umbrella organisation for the recycling industries in Europe. Through its 75 members from 23 European countries, EuRIC represents more than 5,500 large companies and SMEs involved in the recycling and trade of various resource streams. They represent a contribution of 95 billion EUR to the EU economy and 300,000 green and local jobs. By turning waste into resources, recycling reintroduces valuable materials into value chains over and over again. By bridging circularity and climate neutrality, recyclers are pioneers in leading Europe’s industrial transition.

FEAD is the European Waste Management Association, representing the private waste and resource management industry across Europe, including 19 national waste management federations and 3,000 waste management companies. Private waste management companies operate in 60% of municipal waste markets in Europe and in 75% of industrial and commercial waste. This means more than 320,000 local jobs, fuelling €5 billion of investments into the economy every year.